Economists need to make assumptions when they develop models.

Ceteris paribus: hold everything else constant.

Economists cannot conduct scientific experiments because it is impossible to define control variables and independent variables in real life.

1.1.2 Positive and Normative Statements

Positive statements can be tested.

Normative statements are based on opinion.

Economic decisions are often based on value judgement (an educated opinion of what is right or wrong).

1.1.3 The Economic Problem

The basic economic problem is scarcity. There are unlimited wants but limited resources.

Renewable resources can be replenished at the same rate they are being used.

Non-renewableresources cannot be replaced naturally.

Opportunity cost: the value of the next best alternative foregone.

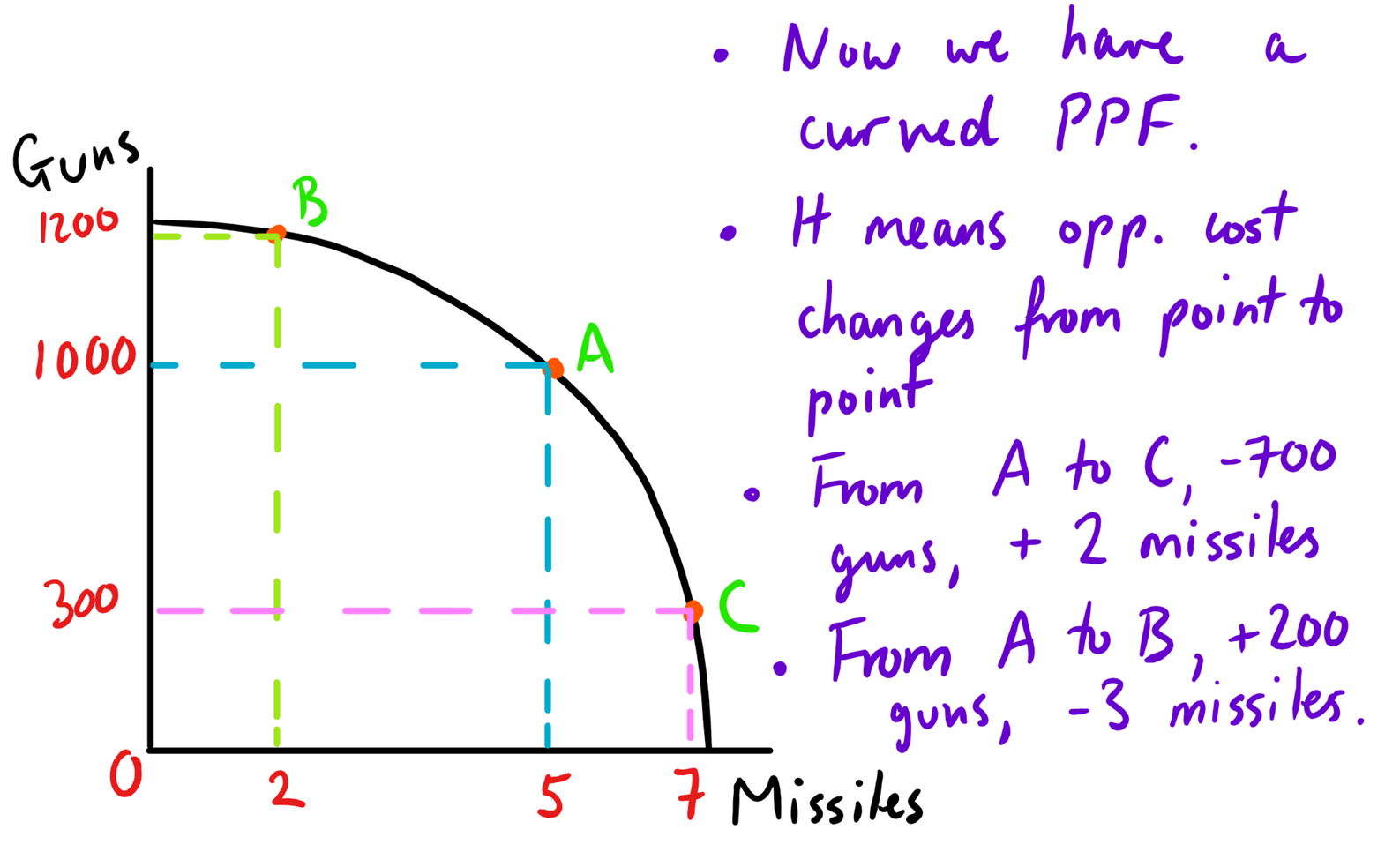

1.1.4 Production Possibility Frontiers

The opportunity cost of being at point C from point A: 700 guns

Any point on the curve shows the maximum productive potential of an economy (efficient allocation of resources).

To produce more of Good A, we have to give up some of Good B. This is opportunity cost. The more of Good A we produce, the greater the opportunity cost increases, as we are giving up more of Good B as the curve becomes cheaper.

Economic growth or decline can be shown by the curve shifting in or out.

A shift in the PPF can be caused by better technology, more resources or greater productivity.

Any point inside the curve is an inefficient allocation of resources.

Any point outside the curve is unattainable.

Capital goods: used to produce other goods and services.

Consumer goods: purchased for personal use and consumption.

1.1.5 Specialisation and the Division of Labour

Specialisation is when an individual/ firm/ nation focuses on producing a specific good or service.

Division of labour is a type of specialisation; when an individual completes/repeats one specific task in a large production process.

Specialisation/ division of labour within a firm

😄 greater productivity (lower costs of production, lower prices)

😦 boring and repetitive tasks (poor job satisfaction could mean lower productivity, workers may leave regularly which increases costs)

😦 workers are vulnerable to structural unemployment (if a job gets automated, they may have lost their other skills)

Specialisation between countries

😄 economic growth and total world output increases (comparative advantage)

😦 countries are vulnerable to economic shocks (Brexit, natural disasters, currency shocks)

Money is a medium of exchange, store of value, measure of value, and a method of deferred payment.

1.1.6 Free Market Economies, Mixed Economy and Command Economy

In a free market economy, there is no government intervention. In a free market, price and quantity is determined by supply and demand (market forces - Adam Smith's invisible hand & Hayek).

😄 price mechanism (changes in demand or supply reflect automatically at the new equilibrium),

😄 no risk of government failure

😦 inequality/ unfairness - the free market only allocates goods and services to those who are willing and able to pay

😦 market failure - the free market doesn't account for externalities

In a command economy, the government allocates all resources (Karl Marx).

😄: less risk of market failure or inequality

😦: risk of government failure

Mixed economy: a combination of a free market and a command economy. There is government intervention in some markets.

Role of state in a mixed economy: government intervention.